- June 8, 2020

- Posted by: CFA Society India

- Category:ExPress

Contributed By: Garish Kansal, CFA

2019 was very good year for financial markets with almost all asset class delivering positive returns with few even delivering double-digit gains including equities (S&P was up by around 30%) and credit segments within fixed income space (including HY, EM and IG debt posting around 13-14% returns). Even the higher quality segments within fixed income including Treasuries and Agency MBS posted around 6-7% returns. This led to stretched valuations across asset classes entering into 2020 as reflected in spreads over Treasuries trading below long-term average (US High Yield and IG credit spreads were around 350bps and 93bps respectively as of Dec 2019), leading to expectations of more of coupon like returns amidst limited scope of further capital appreciation. Driven by concerns around late credit cycle driven by accommodative central banks policies since GFC and stretched valuations, markets were anticipating some correction in 2020 but no one would have anticipated that CoVID19 would be the key trigger for the same as it was earlier expected to be largely contained in China rather than spreading globally.

The speed at which markets reacted to the severe economic shock caused by CoVID19 was extreme as compared to previous sell-off periods like GFC, leading to sharp dislocations across the credit markets including the higher quality segments initially (like Treasuries, IG credits, Agency MBS). US High Yield market also sold off sharply and the extreme impact of the virus was reflected by the fact that High Yield credit spreads took just 23 trading days to widen to over 1000bps in March (touched around 1,100bps on 23rd March from around 360bps as of 20th Feb) as compared to versus 300 days in 2008-09 crisis. However, as the central banks acted quickly by providing massive stimulus in late March and early April, this provided stability to the markets along with improved liquidity conditions specifically for the High Yield bond market which started rallying sharply post Fed announcement on around 9th April including purchase of High Bond ETF as well as fallen angels (bonds which got downgraded from IG to HY rating following 22nd March) which was not used by Fed in 2008/09 crisis. This was reflected in spreads tightening by around 85bps on the day of announcement itself. Since then, there has been continued rally over the last 2 months (High Yield market has recouped YTD losses by ~9% as spreads have tightened further to around 580bps as of 3rd June) driven by optimism around economic recovery owing to easing of lockdown restrictions along with continued central banks support, shrugging off concerns around potential defaults/bankruptcies, dire economic data (around 40mn jobless claims filed since March along with unemployment rate of around 15-20%), surging US China tensions as well as possibility of 2nd wave of infections due to re-opening.

Another important point worth mentioning is that yields in the higher quality fixed income segments (10 year Treasuries remaining range bound at around 60-70bps and IG credit offering around 2-3%) are extremely low and in some cases not even covering keeping up with diminished inflation expectations. This pose significant challenges to the income oriented investors and a result, there could be case for investors to allocate to riskier segments including high yield bonds offering around 7% yields based on current spreads. Having said that, fragility of this recovery also need to be emphasized as there are still downside scenarios with potential for credit markets to face liquidity deterioration despite central bank support. As a result, it would be prudent to maintain cautiously optimistic stance on the high yield credit market. For better understanding, let’s look at the 3 key aspects briefly within the High Yield market – Valuations, Fundamentals and Technical.

Valuations:

Though valuations have tightened by around 500bps since the highs of around 1100bps (witnessed on 23rd March), they are still wider by around 250bps from pre-CoVID levels, thereby offering attractive valuations from capital appreciation perspective along with average coupon of around 6%. Within the various credit quality buckets within High yield, there is lot of dispersion as reflected in CCC rated bonds still trading at around 1500bps as opposed to higher rated BB-B rated bonds which are ranging from 500-700bps, thereby leading to lot of bottom-up relative value opportunities for active managers. Although past performance is not reliable indicator of future performance, history suggest that spreads in excess of 800 bps has provided investors very attractive returns. Once spreads cross 800 bps, the median return over the next 12, 24 and 36 months has been +24.1%, +18.7% and +14.8%, respectively as reflected in previous sell-off seen in 2011 (Eurozone debt crisis) and 2015/16 (Energy sell-off driven by crash in oil prices) when spreads touched around 900bps followed by gradual rally as reflected in Chart 1.

Chart 1: Historical Credit Spread Over Treasuries for ICE BofA US High Yield Index

Source: FRED Economic Research

Fundamentals:

High yield entered this challenging period with low positive growth and reasonable leverage of around 4-5x. However, as the economic impact of virus has been significant with the fastest decline in US GDP, this has led to severe impact on the companies specifically in few of the sectors including travel, leisure, retail along with energy sector which got impacted by weakening demand along with supply concerns (albeit these concerns have abated recently with production cuts with oil prices trading at around USD40 per barrel after briefly going into negative territory in April). As the economic recovery is expected to take several quarters before the growth starts to approach 2019 levels (that too assuming that virus situation would be under control and there is vaccine being developed), this is likely to have huge impact on companies’ earnings and they might have to draw down from bank credit lines along with raising more debt at higher borrowing costs to stay afloat. This is more likely to lead to higher defaults in some of the sectors albeit few of the impacted sectors (airlines, energy, hotels) recently amidst hopes of economic recovery.

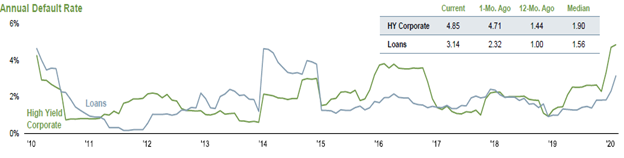

As of May 2020, the last 12 months par-weighted default rate has touched to highest level since GFC to around ~4.85% (vs ~10-11% in 2008/09 crisis and long term average of around 3.6% over the last 30 years) and is projected to increase further to around 7-10%, mostly coming from energy and cyclical sectors. This is also reflected in upgrade to downgrade ratio falling to around 0.4 (as of Apr 2020) vs 0.9 as of end 2019 with around USD40bn of debt getting defaulted on YTD basis as of Apr 20 (vs USD95bn for the full year in 2009). Hence, fundamentals warrant cautious and selective approach. Chart 2 represent the sharp pick up in default rate since end 2019 on LTM rolling basis.

Chart 2: Annual Default Rate for High Yield Bonds and Bank Loans

Source: Eaton Vance

Technical:

Looking at the technical for the high yield market, there is more of mixed story with flows into the asset class along with support from Fed to buy ETFs and fallen angels getting largely offset by surged issuance in April and May (around USD35-40bn issuance) and huge number of downgrades from IG rated names. With expectations of steady issuance over the near term (as companies continually look to bolster the liquidity position) along with accelerated fallen angels (already around USD200bn worth of debt has been downgraded on YTD basis with most notable being Kraft-Heinz, Occidental Petroleum and Ford), High yield market is witnessing the first supply surplus since 2015 after taking into account maturities and rising stars (names moving to Investment grade from High Yield) which might put pressure on bond prices. On the other hand, after witnessing outflows of around USD12bn in March amidst sell-off, the High yield market has seen renewed investors’ interest since early April as reflected in nine consecutively weekly inflows totaling around USD36bn. Worth noting that 5 of the 10 largest weekly inflows on record have occurred over this nine-week stretch.

Conclusion

Although US Treasury and Fed has followed “whatever it takes” approach to provide stimulus to support economic recovery and providing liquidity to the market leading to the sharp rally since March sell-off, many companies are likely to face bankruptcies/restructuring amidst expectation of uneven recovery in economic growth. Having said that, there would be clear differentiation between winners and losers going forward within the High yield corporate credit space and active managers can look to find good relative value opportunities across sectors based on bottom-up security selection by focusing on companies with strong balance sheet, good access to capital and ability to weather the uncertain economic environment.

As a result, given the attractive valuations along with reasonable fundamentals and technical picture, investors can follow cautiously optimistic approach towards taking credit risk and can look to add exposure to High Yield asset class by selecting active managers following conservative investment approach structurally (via maintaining adequate liquidity, focusing on higher rated BB-B bonds along with defensive non-cyclical sectors with stable cash flows) but hold flexibility to add risk by taking tactical allocation to lower rated CCC bonds (trading at very cheap valuations) as well as identifying bottom-up opportunities in sectors facing secular headwinds. This approach is likely to allow the investors to participate in the upside in case the current rally continues but with the ability to protect downside as well in case there is another dislocation in credit markets along with deterioration in liquidity conditions.

About the Author:

Garish Kansal has 12 years of industry experience in the financial markets across diverse fields mainly Fund Research/Manager Research and Credit Research. He is currently working with HSBC for the last 6.5 years leading the Fixed Income Mutual Fund Research efforts to support Global Wealth Business through approval and recommendation of 3rd party mutual funds, ETFs, Separately Managed Accounts and Fixed Maturity Products. Prior to HSBC, he has worked at AMBA Research (a Moody’s subsidiary) and DE Shaw responsible for covering Credits for buy side portfolio managers. His area of interest includes Manager Research, Economic Research, Trends in asset management industry, ESG in Fixed Income, and Portfolio Performance analysis across fixed income asset classes. He is a CFA Charter holder and has done MBA Finance from ICFAI Hyderabad.