- February 2, 2014

- Posted by:

- Category:BLOG, Events

Contributed by: Meera Siva

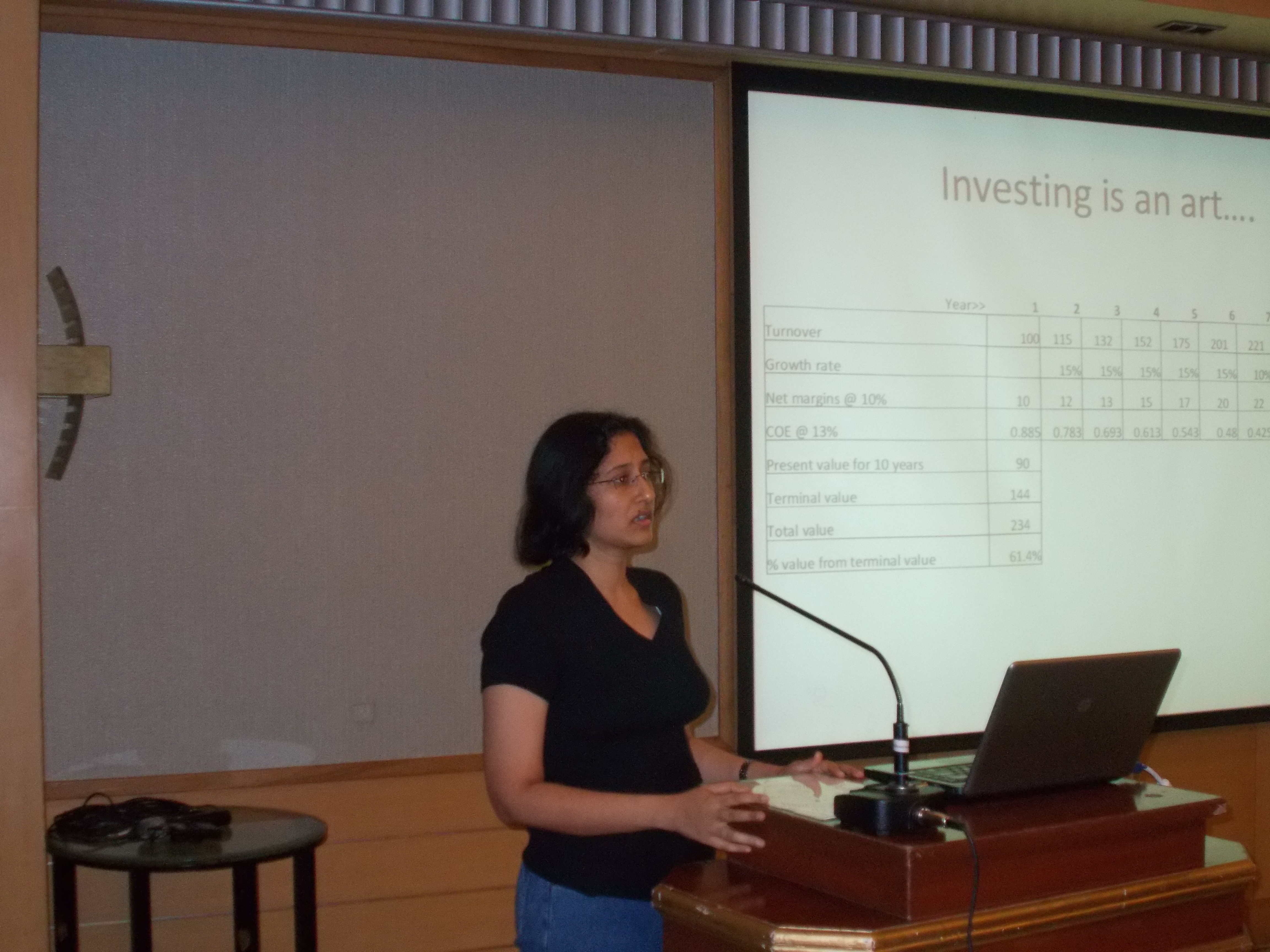

Ms Roshi Jain, who is the VP and Portfolio Manager – Equities for Franklin Templeton India AMC (FT), spoke on how stock picking is an art and involves more than DCF analysis. She drew upon her experience of 11 years in the investing industry comprising of a portfolio manager of two FT funds and co-portfolio manager of two other FT funds along with her prior experience at Goldman Sachs to highlight key aspects of picking multi-baggers. She stressed that financial models are based on assumptions and the result ultimately depends on our judgement. The terminal value accounts for about 60 per cent of the value of a firm in DCF analysis hence we need to refine our assumptions if we want to pick right. She explained with practical examples of companies that did well and returned good value to shareholders.

Her first example was Asian Paints which has returned an average of 34 percent per year in the last 10 years. So, Rs 1,000 invested in January 2004 would have grown to Rs 18,360 now. Some important strengths of the company – distribution edge, reducing inventory using tinting machine and branding whereby paint was not seen as commodity – helped Asian Paints to be a winner. Financially too the company has maintained steady margins of 15 to 17 percent, is debt free and pays out 40% of profits as dividends.

She then highlighted Titan which has returned 47 percent per annum in the last 10 years despite company’s attempts to expand abroad failed. Titan identified the trust gap which buyers had in jewellery stores and the Tata name helped them win credibility. Their model of hedging gold price risk through gold lease has helped earn stable returns while others in the same industry had volatile returns – something the market does not like. She said that while Titan and Asian Paints do not have debt, leverage is not always bad. Banks have high leverage which helps them amplify returns. She cited the example of HDFC bank that has been consistently delivering good results because of its discipline in lending and the strength of its sticky retail customers.

How about avoiding the trap of buying a bad stock on a good story? She said high leverage model such as the one used in the infra sector where the promoter has connection to wins projects and even the equity is funded by debt taken by subsidiaries leads to trouble when downturn strikes. So it is important to note that many stories can go wrong and the models that can weather a downturn are the ones that can sustain growth when things improve.

– M S