- May 26, 2026

- Posted by: CFA Society India

- Category:BLOG, ExPress

Dr. Shagun Thukral, CFA

Adjunct Faculty and Senior Investment Professional

More Indian retail investors are moving into equities and higher-risk credit. Some of this reflects genuine financial deepening. But a large part is driven by a simpler reality: safe investments no longer pay enough after tax and inflation. This article looks at the tax gap between debt and equity, what it does to real returns, and how it is quietly distorting household savings. It also assesses policy ideas that could restore balance without rolling back India’s emerging equity culture.

1. A Widening Tax Asymmetry

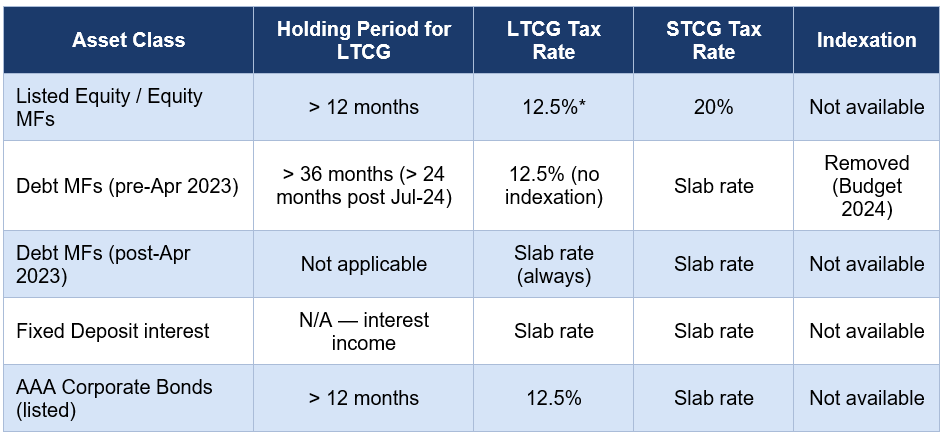

India’s tax code treats equity and debt very differently and the gap has widened sharply since 2023. The table below shows where things stand for key asset classes in FY 2025-26:

*Annual exemption of ₹1.25 lakh applies to equity LTCG under Section 112A. STCG on listed equity raised from 15% to 20% effective 23 July 2024. Sources: Income Tax Act 1961, Finance Act 2023, Finance Act (No.2) 2024, CBDT notifications.

Before April 2023, debt mutual funds held for over three years qualified for a 20% LTCG rate with indexation which was meaningfully better than FDs, where all interest is taxed at slab rates. The Finance Act 2023 changed this through Section 50AA. Gains from debt mutual funds bought on or after 1 April 2023 are now always treated as short-term and taxed at the investor’s slab rate, regardless of how long the fund is held. Budget 2024 went further, removing indexation from most other long-term assets too.

The result is stark. Holding a debt fund for ten years now produces the same tax bill as holding it for ten months. A long-tenure debt fund and a bank FD are, for tax purposes, identical.

2. The Real Returns Problem

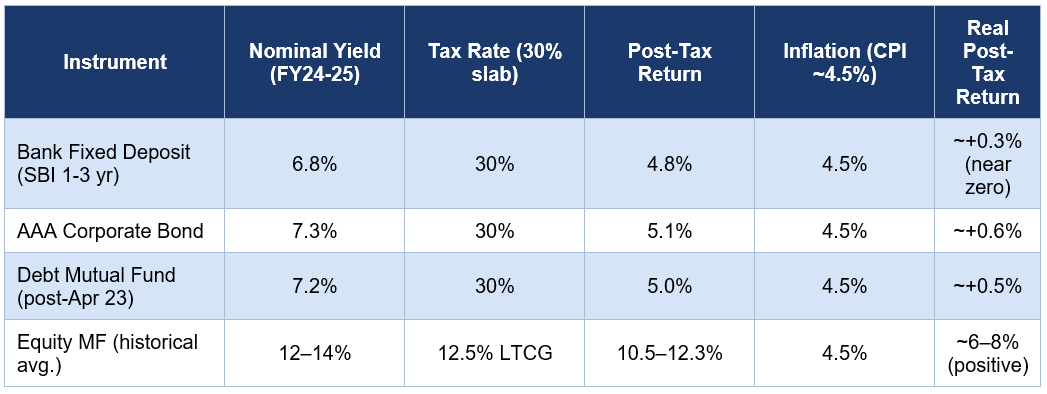

While nominal yields appear attractive, what matters is what you actually keep after paying tax and watching inflation erode purchasing power. The table below shows how this plays out for a 30% bracket investor in FY 2024-25:

(FD rate based on SBI 1-3 year tenure (6.8% as at early FY25). Equity MF based on historical Nifty 50 average; LTCG rate of 12.5% applied post July 2024. CPI inflation of ~4.5% reflects RBI’s FY25 estimate. Figures are illustrative; actual post-tax returns depend on individual tax profile and market conditions. Sources: SBI deposit rates, RBI Monetary Policy Report, AMFI, Income Tax Act.)

For retirees and conservative savers living off fixed-income products, near-zero real returns are not merely disappointing but represent a structural tax on prudence. In years when CPI is elevated, even a positive nominal yield can mean a negative real return after tax.

Taxing nominal gains without adjusting for inflation means the government is often taxing the return of capital, not the return on it. The careful saver ends up worse off in real terms.

3. Where the Money Is Going

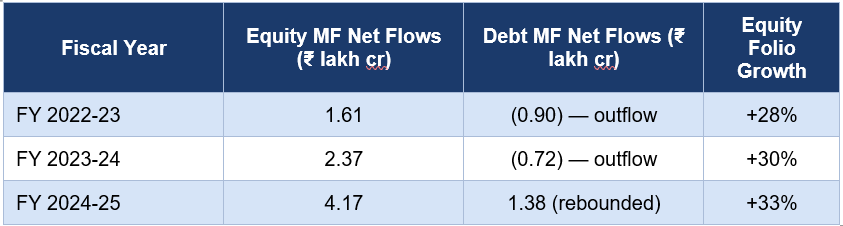

The numbers tell the story. Equity fund inflows have surged; debt funds saw three straight years of outflows before a partial recovery in FY25:

Sources: AMFI Annual Report FY2025; Business Standard (19 May 2025). Debt fund FY25 rebound was driven primarily by expectations of RBI rate cuts (repo rate reduced 125 bps in 2025 to 5.25%) and yield declines, not a reversal of tax-driven structural flows

In FY25, equity funds attracted ₹4.17 lakh crore, three times the ₹1.38 lakh crore that went into debt. Equity folios rose 33% to 16.38 crore; debt folios actually shrank 3% to 6.95 crore. By March 2025, equity schemes accounted for roughly 70% of all mutual fund folios.

In addition, online bond platforms have made corporate bonds far more accessible offering lower ticket sizes and simpler onboarding. That’s a good thing. But access without suitable understanding creates its own risks. When investors who once preferred FDs start buying AA- or A- rated bonds mainly because safe alternatives no longer yield enough, that’s not a confident choice. It’s a reluctant one.

Many retail investors entering higher-yield credit may not fully grasp downgrade risk, illiquid secondary markets, or what happens in a default. Yield-chasing born of necessity is not the same as informed risk-taking.

4. The Policy Uncertainty Problem

Long-term investing is built on predictability. People allocate money based on the tax rules in place at the time they invest. When those rules change after the fact, trust erodes.

The 2023 removal of indexation from debt mutual funds caught many investors off-guard. They had committed to multi-year allocations under a very different tax assumption. Budget 2024 then extended the removal of indexation to other asset classes. Repeated changes, arriving in quick succession, make it harder for anyone to plan with confidence.

India wants deeper capital markets and greater household participation in financial savings. That ambition needs a stable policy environment to rest on. Policy predictability is itself a form of institutional capital.

5. Tax Policy and the Khan Committee’s 7I Framework

The most enduring framework for developing India’s corporate bond market comes from the 2016 Khan Committee Report (RBI Working Group on Development of Corporate Bond Market in India). It organised its recommendations around seven pillars or the 7I Framework. These were – Issuers, Investors, Intermediaries, Infrastructure, Incentives, Instruments, and Innovations.

Tax policy belongs squarely in the Incentives pillar. The Report envisaged this pillar working through fiscal and regulatory measures such as stamp duty rationalisation, credit enhancements, and steps to broaden investor participation. Yet nearly a decade later, tax policy has moved the other way. The removal of indexation from debt mutual funds and the absence of any preferential treatment for long-tenor corporate bond investments have weakened, not strengthened, this pillar.

NITI Aayog’s December 2025 report on deepening the corporate bond market calls for “targeted incentives” to expand retail participation but the most direct lever, tax parity, remains untouched. India’s corporate bond market is about 16% of GDP; equity markets are seven times its size. All seven pillars of the 7I Framework need to pull together. A tax environment that discourages fixed-income investing undermines both the Investors and the Incentives pillars at once.

The goal here is not to use tax to push retail investors toward corporate bonds as that would just swap one distortion for another. It is to stop tax from being an active deterrent. When investors move into lower-rated bonds not because they understand the risks but because safer options yield nothing real, bond market participation becomes fragile, not deep.

6. The Case for Tax Neutrality

The argument here is not against equity or against the retail equity wave. It is simpler: investors should choose how much risk to take based on their goals and circumstances and not because the tax system has made safe options unworkable.

Tax neutrality means comparable tax treatment for investments with comparable economic roles, so that asset allocation is driven by risk appetite rather than tax arbitrage. Right now, that principle is being violated.

Some measures worth considering could be:

- A concessional LTCG rate for long-hold debt: apply a flat 12.5% rate (matching equity LTCG) to gains on listed corporate bonds and debt mutual funds held beyond 36 months. No need to restore indexation but just introducing holding-period sensitivity, as exists for equity.

- Extend the ₹1.25 lakh annual LTCG exemption to qualifying corporate bond gains. Currently available only for equity under Section 112A, extending it to long-term debt is regime-neutral and directly benefits smaller retail investors.

- Stronger grandfathering when rules change: investors need to know that the tax assumptions under which they commit capital will hold. Retrospective changes should be the exception, not the pattern.

- Clearer SEBI and AMFI suitability norms for retail investors accessing sub-investment-grade bonds through digital platforms so that broader access does not become a route to unsuitable risk-taking.

The common thread here is to widen the space for informed, appropriate participation across the risk spectrum. Tax policy should be neutral between asset classes and not a thumb on the scale.

Conclusion

India’s financial markets have evolved in many ways such as rising SIPs, broader retail participation, and better access to bonds through digital platforms. But when the tax and inflation environment makes safe investing unviable, the shift toward equity and high-yield credit reflects distorted incentives as much as genuine confidence.

A healthy financial system gives investors a real choice across the risk spectrum. When prudence stops paying, that choice disappears.

The goal is simple: investors should take risks because they want to, not because the tax code leaves them no other option.

Sources: Finance Act 2023, Finance (No.2) Act 2024, Income Tax Act 1961, AMFI Annual Report FY2025, RBI Monetary Policy Reports, CBDT Notifications, ClearTax, Finnovate Research.

Disclaimer:

The views and opinions expressed in this article are solely those of the author and do not necessarily reflect the official position of CFA Society India. The content is intended for informational purposes only and should not be construed as financial, investment, legal, or professional advice.

Readers are encouraged to consult qualified experts before making decisions based on the information provided. While efforts have been made to ensure the accuracy and timeliness of the content, no guarantees are offered regarding its completeness or reliability. The author and CFA Society India will not be held responsible for any errors, omissions, or outcomes related to the use of this material.

By accessing and reading this article, you acknowledge and agree to this disclaimer.

About the Author:

Shagun is a Doctorate, CA and a CFA with over 20 years of experience in the investment industry. She was recognised as one of India’s Top 100 Women in Finance by AIWMI in 2019. Shagun started her career as part of a buy-side fixed income team at a leading insurance company, working in various capacities including credit analyst and fund manager. After 7 years, she moved to the education industry with a keen interest in bringing real-world and application based learning to the classroom. She teaches subjects like Financial Markets, Financial Accounting, Fixed Income and Wealth Management. While continuing as an Adjunct Faculty, she moved on to an entrepreneurial role of a wealth manager managing investments for retail and HNI clients. She also conducts sessions and workshops on financial awareness for individuals. Having a passion for bond markets, she completed a Ph.D in Corporate Bond Markets in India in 2020 and has published several research papers and case studies in both national and international journals.