- June 1, 2013

- Posted by:

- Category:BLOG, Events, Speaker Events

The Indian Association of Investment Professionals (IAIP) organized a knowledge and experience sharing session presided by Bud Haslett CFA FRM, Executive Director – Research Foundation of Chartered Financial Analyst Institute at Bangalore on May 17th 2013. The session covered various topics such as the general derivative markets and trends, options review, determinants of options premiums, risk measurement, options strategies, delta hedging and volatility strategies. The event was well received by the members. The followings are the key takeaways from this event.

Derivatives Overview

Derivatives are traded in two types of markets: Over the Counter (OTC) and Exchange Traded. Each market has its unique way of operating. Following are the characteristics of respective markets:

| OTC | Exchange Traded |

| Flexible Terms | Standardized Terms |

| Mostly Low Transparency | Transparency |

| Mostly No Central Clearing | Centralized Clearing |

| Generally Unregulated | Regulated |

Exchange traded products offer some benefits over the OTC traded products like one central counterparty, liquidity and transparency. As a result of these benefits, trading on organized market has increased many folds over the years.

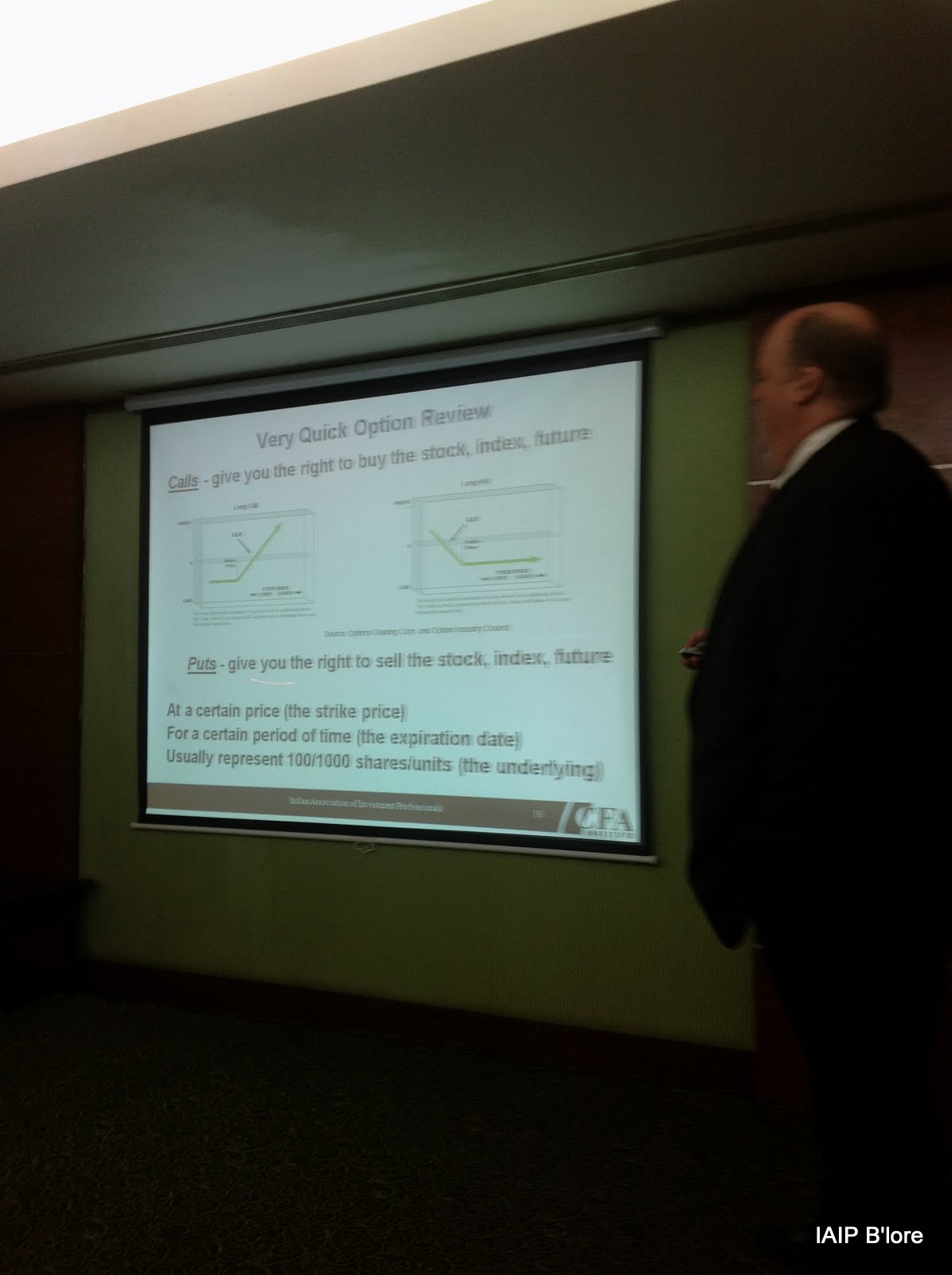

Options Review

Call option gives the right to buy the stock, index and future whereas Put options gives the right to sell the stock, index and future:

- At a certain price (the strike price)

- For a certain period of time (the expiration date)

- Usually represent number of shares per unit (the underlying)

An investor has to pay an amount to buy these contracts which is called option premium.

Valuing the Option

Bud explained that options can be valued using Balck-Scholes, binomial and other models. However, Black-Scholes Model (BSM) is widely used by the market to value options. BSM is set up on the following assumptions: lognormally distributed, risk free rate is constant, volatility is known and constant, no taxes or transaction costs, European style options.

American style options can’t be valued using BSM. Underlying premise in the American style options is that option can be exercised at any time or at any price during the contract period. On the contrary, European options can only be exercised at strike price on the expiration date. Initially, BSM model assumed that there will not be any cash flows on underlying. However, BSM was subsequently modified to include cash flows on underlying (e.g. dividends). BSM model relies on following inputs to calculate the value of the option: stock price, interest rate, strike price, dividends, time, and volatility.

Value of a call option will increase with the increase in these inputs except the increase in strike price and dividends. With an increase in strike price and dividends, price of option will come down. A put option will increase in value with the increase in all inputs except stock price and interest. Increase in stock price and interest will decrease the value of put option.

At this point, Bud noted that position simulator tool on http://www.optionseducation.org is a great tool to understand the impact of changes in all these inputs on option price. It calculates price of option based on input provided by the user.

Option Greeks

Movement in option price can be explained using following option Greeks:

- Delta: change in option price based on stock price changes. For call options, delta range from 0.00 to 1.00. Whereas for put options, it range from negative 1.00 to 0.00.

- Gamma: change in delta of stock based on stock price changes

- Theta: change in option price based on time change

- Vega: change in option price based on volatility

- Rho: change in option price based on change in interest

As options near expiration, delta moves closer to 1.00. This means higher chances of changes in option price in tandem with movement in stock price.

Delta Hedged Position

Under delta hedge, delta is adjusted by going long (buying) and short (selling) on same underlying in such a way that delta of a position is zero. In such a position, value of option doesn’t change with small changes in stock price of underlying.

- Short Gamma position: Investor shorts more options than going long. Holder will lose with increase or decrease in stock price but makes money as time passes.

- Long Gamma position: Investor long more option than shorting. Holder will make money with increase or decrease in stock price but loses money as time passes.

Option Strategies

- Covered Call: This strategy is combination of going long on stock and simultaneously shorting call on the same stock. This strategy limits upside participation but holder gains as time decay. Time decays means that value of options fall as time passes and option reaches its expiration.

- Protective Put: In this strategy, holder will go long on stock and takes long put position. This strategy limits downside losses but holder loses as time passes.

- Collar: Collar combines covered call and protective put. Investor will go long stock, buys a put and shorts call. This strategy protects from short term weakness.

- Covered Call Writing: This strategy combines long stock position with selling call option on same stock. Holders collects premium from writing the call. In this strategy, upside is capped at strike price + premium whereas downside risk is not eliminated.

Volatility Strategies

Higher volatility results into greater movement (on either side) in price of underlying. This also leads to higher option premiums both for put and call. Volatility measures changes in underlying stock price.

- Long Straddle: It is a combination of long call and long put at same strike price and expiration. This results into profit if stock price moves sharply in either direction.

- Long Strangle: This is combination of long call and long put with the same expiration but call strike price is higher than put strike price. This position gives same benefit but at the lower cost than Long Straddle.

Bud concluded that utilizing options have both positives and negatives. Positives are leverage, time decay and limited risk and negatives are leverage, time decay and unlimited risk. Investor needs to understand that for every positive there is negative. They need to play in such a way that positives are valuable to them than the negatives.

Contributed by: Deepak Mundra CFA

Photo Courtesy: Abhimanyu Laxman

Very nice tips for risk management. Very nice and informative information. hanks for sharing this experience here.

Hello mate, very nice and informative article you have shared with all of us. I appreciate your efforts. Thanks

I was curious if you ever thought of changing the page layout of your website? Its very well written; I love what youve got to say. But maybe you could a little more in the way of content so people could connect with it better. Youve got an awful lot of text for only having one or two images. Maybe you could space it out better?

Keep up the very good work.